On 1 October 2013, Penketh acquired 90 million of Sphere’s 150 million $1 equity shares. T

The retained earnings of Sphere brought forward at 1 April 2013 were $120 million.

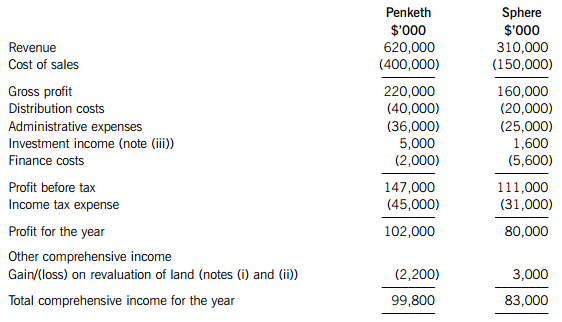

The summarised statements of profit or loss and other comprehensive income for the companies for the year ended 31 March 2014 are:

The following information is relevant:

(i) A fair value exercise conducted on 1 October 2013 concluded that the carrying amounts of Sphere’s net assets were equal to their fair values with the following exceptions:

– the fair value of Sphere’s land was $2 million in excess of its carrying amount

– an item of plant had a fair value of $6 million in excess of its carrying amount. The plant had a remaining life of two years at the date of acquisition. Plant depreciation is charged to cost of sales.

– Penketh placed a value of $5 million on Sphere’s good trading relationships with its customers. Penketh expected, on average, a customer relationship to last for a further five years. Amortisation of intangible assets is charged to administrative expenses.

(ii) Penketh’s group policy is to revalue land to market value at the end of each accounting period. Prior to its acquisition, Sphere’s land had been valued at historical cost, but it has adopted the group policy since its acquisition. In addition to the fair value increase in Sphere’s land of $2 million (see note (i)), it had increased by a further $1 million since the acquisition.

(iii) On 1 October 2013, Penketh also acquired 30% of Ventor’s equity shares. Ventor’s profit after tax for the year ended 31 March 2014 was $10 million and during March 2014 Ventor paid a dividend of $6 million. Penketh uses equity accounting in its consolidated financial statements for its investment in Ventor.

Sphere did not pay any dividends in the year ended 31 March 2014.

(iv) After the acquisition Penketh sold goods to Sphere for $20 million. Sphere had one fifth of these goods still in inventory at 31 March 2014. In March 2014 Penketh sold goods to Ventor for $15 million, all of which were still in inventory at 31 March 2014. All sales to Sphere and Ventor had a mark-up on cost of 25%.

(v) Penketh’s policy is to value the non-controlling interest at the date of acquisition at its fair value. For this purpose, the share price of Sphere at that date (1 October 2013) is representative of the fair value of the shares held by the non-controlling interest.

(vi) All items in the above statements of profit or loss and other comprehensive income are deemed to accrue evenly over the year unless otherwise indicated.

Required:

(a) Calculate the consolidated goodwill as at 1 October 2013.

(b) Prepare the consolidated statement of profit or loss and other comprehensive income of Penketh for the year ended 31 March 2014.

The following mark allocation is provided as guidance for this question:

(a) 6 marks

(b) 19 marks

如搜索结果不匹配,请 联系老师 获取答案

如搜索结果不匹配,请 联系老师 获取答案