题目内容

(请给出正确答案)

[主观题]

Under U.S. GAAP what is the most likely effect of the reversal of a valuation allowan

ce related to a deferred tax asset on net income?

A. No effect

B. A decrease

C. An increase

如搜索结果不匹配,请 联系老师 获取答案

如搜索结果不匹配,请 联系老师 获取答案

A. No effect

B. A decrease

C. An increase

如搜索结果不匹配,请 联系老师 获取答案

更多“Under U.S. GAAP what is the mo…”相关的问题

更多“Under U.S. GAAP what is the mo…”相关的问题

第1题

Is the reversal of an inventory write-down permitted under U.S. GAAP (generally accepted accounting principles) and International Financial Reporting Standards (IFRS)?

A. No, under both

B. Yes, under both

C. Yes under IFRS but not under U.S. GAAP

第2题

A. reduction in tax rates.

B. decrease in interest rates.

C. increase in the carry forward periods available under the tax law.

第3题

Two software companies that report their financial statements under U.S. GAAP (generally accepted accounting principles) are identical exceptas to how soon they judge a project to be technologically feasible. One firm does so very early in the development cycle while the other usually waits until just before the project is released to manufacturing. Compared to the company that judges technological feasibility early, the one that waits until closer to manufacturing willmost likely report lower:

A. financial leverage.

B. total asset turnover.

C. cash flow from operations.

第4题

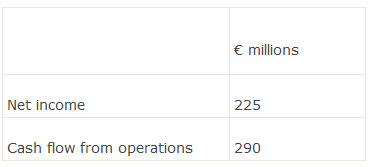

A European based company follows IFRS (International Financial Reporting Standards) and capitalizes new product development costs. During 2008 they spent€25 million on new product development and reported an amortization expense related to a prior year’s new product development of €10 million. Other information related to 2008 is as follows:

An analyst would like to compare the European company to a similar U.S. based company and has decided to adjust their financial statements to U.S. GAAP. Under U.S. GAAP, and ignoring tax effects, the cash flow from operations (€ millions) for the company would be closest to:

A. 265.

B. 275.

C. 290.

第5题

第6题

A. grows primarily through acquisitions.

B. develops its patents and processes internally.

C. invests a substantial amount in new capital assets.

第7题

Assume U.S. GAAP (generally accepted accounting principles) applies unless otherwise noted.

A company has equipment with an original cost of $850,000, accumulated amortization of $300,000 and 5 years of estimated remaining useful life. Due to a change in market conditions the company now estimates that the equipment will only generate cash flows of $80,000 per year over its remaining useful life. The company’s incremental borrowing rate is 8 percent. Which of the following statements concerning impairment and future return on assets (ROA) is most accurate? The asset is:

A. impaired and future ROA increases.

B. impaired and future ROA decreases.

C. not impaired and future ROA increases.

第8题

A company prepares its financial statements in accordance with U.S. GAAP (generally accepted accounting principles). It expected to be the sole supplier for a state-wide school milk program and had production facilities valued at $28.4 million. Recently several other companies were also granted milk-supply contracts throughout the state and the company now estimates that it will only be able to generate cash flows of $3 million per year for the next 7 years with its facilities. The firm has a cost of capital of 10%.

The impairment loss (in $-millions) on the production facilities will most likely be reported in the company’s financial statements as a:

A. 13.8 reduction in operating cash flows. .

B. 13.8 impairment loss in the income statement

C. 7.4 reduction in the balance sheet carrying amount.

第9题

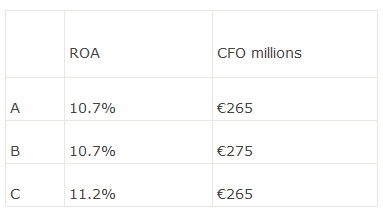

Lazlo Ltd, a European-based telecommunications providers, follows IASB GAAP and capitalizes new product development costs. During 2012 they spent €25 million on new product development and reported an amortization expense related to a prior year’s new product development of €10 million. Other information related to 2012 is as follows:

An analyst would like to compare Lazlo to a US-based telecommunications provider and has decided to adjust their financial statements to U.S.GAAP. under U.S.GAAP, and ignoring tax effects, the return on asset (ROA) and cash flow from operations (CFO) for Lazlo would be closestto:

第10题

Moreover, the traffic-safety agency estimates that even among parents who always strap their children in, 85% are not doing it properly. They often don't know where best to place the kids, don't use the proper restraint for their age and weight, or don't install the safety seats properly. Despite the reports about front seats collapsing onto back seats when certain car models get in accidents, the safest place in the car for any child up to the age of 12 is still the back seat. Babies up to 9 kg and one year old should ride in rear-Facing infant seats.

Never place a child under age 12 in the front seat with a working passenger-side air bag. These devices are discharged at 320 km/h and can be triggered by low-speed fender benders. They have killed 77 kids in the U.S. since 1993. If you must place a child in front, make sure the paasengar-side bag is switched off.

Children over age one should ride in forward-facing safety seats with a five-point harness system. A child who weighs at least 18 kg or at least 1m high can graduate to a booster seat that elevates her so that the standard shoulder and lap belt fits properly.x

What does the author mainly discuss in this passage?

A.How to avoid car crash.

B.How to design safer baby equipment.

C.How to educate children properly.

D.How to properly secure children in the ear.

为了保护您的账号安全,请在“赏学吧”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!

微信搜一搜

微信搜一搜

赏学吧

微信搜一搜

赏学吧

赏学吧

微信搜一搜

赏学吧